Down Payment: How Much is Enough?

The down payment you put towards your home is a huge factor in the homebuying equation. The budget you set for your down payment will determine your home price, how long it’ll take to save up for your home, and even the types of mortgages you may qualify for.

What is the minimum down payment to buy a home?

So how much is actually required? It depends!

If you’ve heard that you should put at least 20% down on a new home, you’re not alone. While putting a higher amount down is beneficial, it’s not necessary.

Based on your loan type, you may be required to put a certain percentage of the home’s price down to qualify for your mortgage.

-

Conventional Loan: Minimum 3% down

-

FHA Loan: Minimum 3.5% down

-

Jumbo Loan: Varies; ask your Loan Officer

While these are the minimum requirements for each loan program, not all borrowers will qualify for the minimum down payment. For example, to put down the minimum of 3.5% on an FHA loan, the borrower would need a credit score of at least 580. A lower credit score would raise the minimum required down payment.

Which mortgage requires the lowest down payment?

If you’re looking for a low down payment, you’ll want to consider a USDA loan or a VA loan if you qualify.

USDA loans are available to those who meet certain income and location requirements. If you're purchasing a home in an area designated for USDA loans, you may qualify for a mortgage with no down payment.

VA loans are only available to qualifying active-duty service members, veterans, reserve members, National Guard members and eligible surviving spouses. Additionally, you must have sufficient credit and income and a valid Certificate of Eligibility (COE). Qualifying borrowers may be eligible for a VA loan with no down payment.

If you’re not eligible for either a USDA or VA loan, ask your Loan Officer if a conventional or FHA loan would be better for you. Down payments requirements may change based on your debt-to-income ratio, credit score and more, so it’s essential to compare your specific situation to find out which option is best for you.

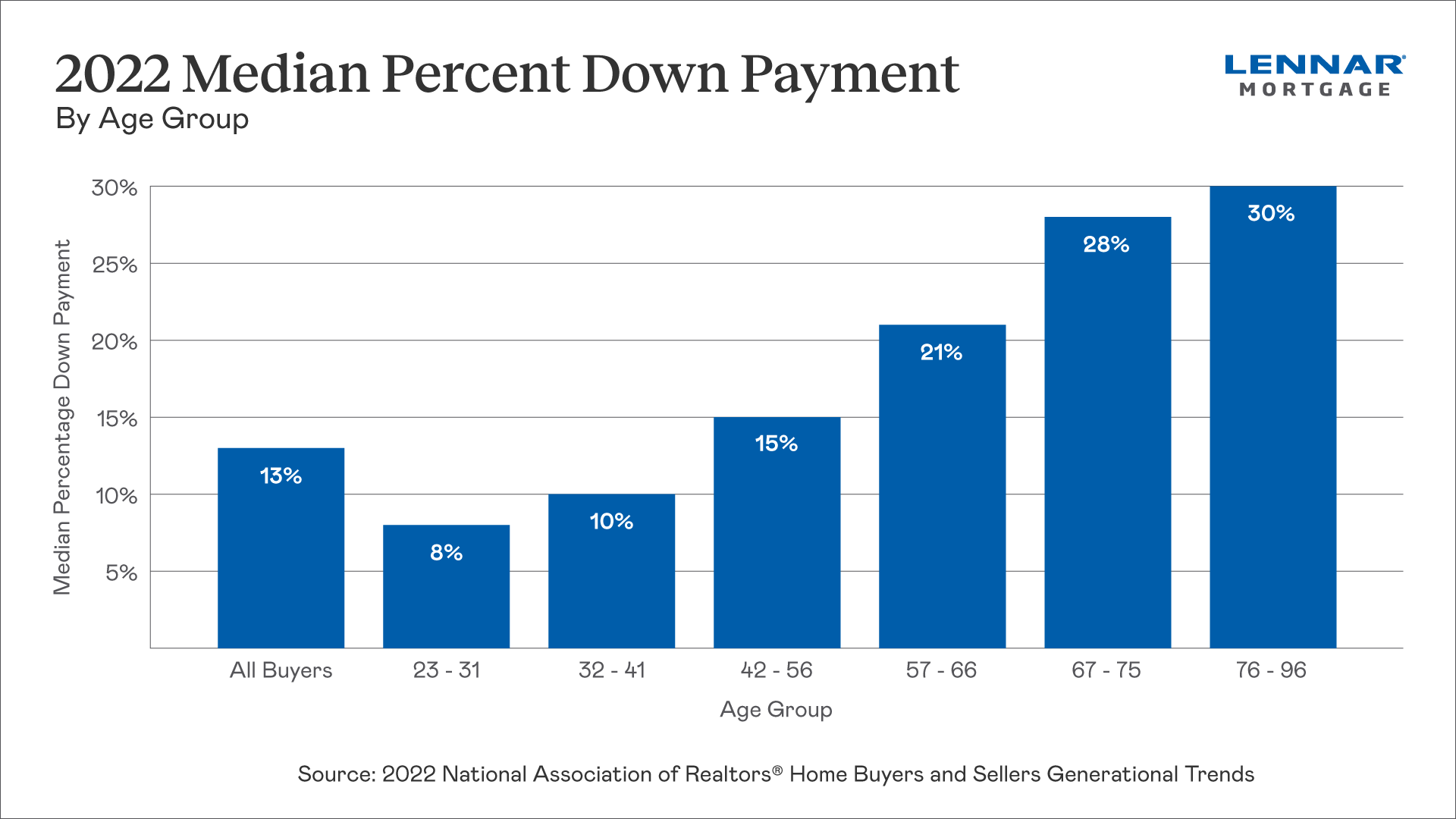

What is the average down payment in America?

The National Association of Realtors reports that the typical down payment for first-time buyers is 6% and the typical down payment for repeat buyers is 17%.

The NAR’s research shows that the median down payment for all buyers is 13%. When buyers are separated out by age group, we see a trend of younger buyers having lower down payments.

When saving up for your down payment, be sure to factor in closing costs as well. These fees, usually amounting to about 2% - 5% of the purchase price, will also need to be paid at closing.

What is the benefit of putting over 20% down on a home?

You may have heard that homebuyers should be aiming to put at least 20% down on their home. While that number may not be realistic for many buyers, there are benefits to a down payment of at least twenty percent.

On top of reducing your loan value, a 20% down payment means you won’t need private mortgage insurance (PMI). Mortgage insurance is required for lower down payments and adds to your total monthly payment. If you start with a lower down payment, you can remove your private mortgage insurance after you’ve reached 20% equity in your home.

Are there programs that offer down payment assistance?

Yes! There are a variety of down payment assistance options that can help you get into a home. Your eligibility for various programs will depends heavily on your location. To learn more about programs available in your state, you can browse the resources listed by the Department of Housing and Urban Development.

According to the National Association of Realtors, first-time homebuyers made up just 26% of all homebuyers in 2022 – the lowest percentage since data collection began. Many assistance programs are targeted specifically at this audience, with the aim of increasing homeownership overall.

Be sure to ask your Loan Officer what down payment assistance you qualify for!

How does my down payment affect the total amount I'll pay?

Saving for a down payment is often one of the hardest steps of buying a home. However, paying less up front could cost you more in the long run.

The less you put down on a home, the higher your monthly payment will be. On top of that, a down payment of less than 20% will require private mortgage insurance, adding even more to your monthly costs. Finally, a lower down payment may lead to higher interest rates from lenders.

Overall, you will likely pay more over the lifetime of your home loan if you choose to minimize your down payment. If possible, try to calculate your monthly payment early on in the process. Setting a savings goal for your down payment and a budget for your home price can help you make smart financial decisions when it’s time to buy.

Which loan option should I choose?

Taking on a mortgage is an important decision. With many options and scenarios to compare, our Loan Officers are here to help you decide which loan is right for you.

We provide the simplest path to homeownership – ensuring you have guidance each step of the way – for those interested in owning a Lennar home. Get pre-qualified today to get started!